The Buyability Gap: A Hidden Cost of Your AI Product Growth

Measure what buyers can verify about your product before they engage sales.

TL;DR

Growth stalls when product capability outruns commercial legibility. We analyzed 60 AI-native and AI-powered B2B products across 8 buyer-confidence dimensions. The market is splitting into two camps: gated companies that route everything through sales, and buyable companies that publish the value unit, make cost drivers legible, and let buyers build a business case independently. The single biggest separator between top and bottom scorers: whether the company had defined and published its value unit. Every top scorer had one. None of the bottom scorers did. Most companies already have the information internally. The gap is not capability. It is legibility.

A VP of Engineering finds a tool that cuts her team's deployment time in half. She runs a pilot. Her developers love it. She brings it to procurement with a strong recommendation. Then the procurement manager asks: What does it cost at 200 seats? What happens if usage spikes? How do overages work? What controls exist for budget limits?

She checks the vendor's site. The pricing page says "contact us." The docs describe what plans cover but say nothing about cost drivers or control mechanisms. There is no way to model the spend at scale.

The deal stalls. Not because the product failed, but because the champion could not build a business case easily. In this case, it took six more weeks for the deal to finally go through. However, more often, the evaluation never reaches sales. In B2B, doing nothing is always the lowest-risk option.

That is the Buyability Gap.

Buyability is the degree to which a buyer can independently understand, evaluate, budget for, and justify a product without engaging a vendor's sales team.

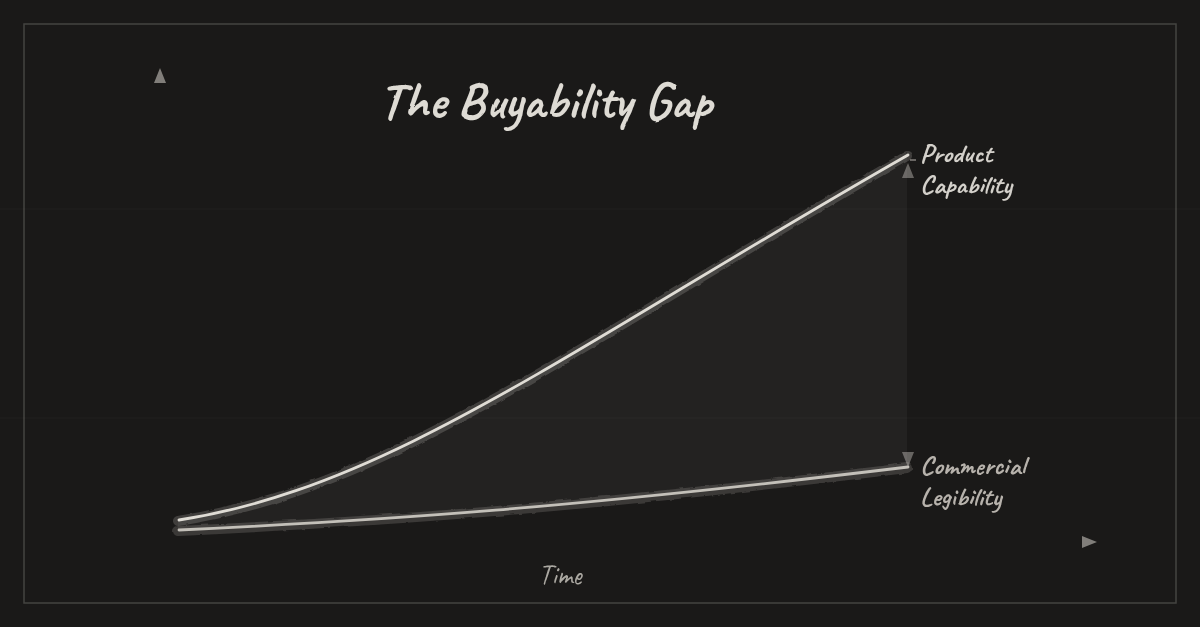

As product capability accelerates, commercial legibility often falls behind. The widening gap between the two is where deals stall, evaluations go silent, and growth slows without a clear signal why.

Why this is structural now

Rati Zvirawa, Senior Director of Product at Intercom, put it plainly in the GTM Atlas by Attio: "In 2026, the buyer has changed. The seller hasn't."

Buyers are now deploying AI agents to evaluate vendors before any human conversation starts. An agent cannot read between the lines. It cannot see behind a "contact us" wall. When an agent evaluates your product and finds nothing to verify, the gap was already there. As Rati put it: "The Agent didn't break the metric. It surfaced that the metric was already broken."

What we found

We built the AVS Rubric to measure the trust infrastructure that enables buyability. It scores products across eight buyer-confidence dimensions, from pricing clarity and cost driver mapping to operational controls and compliance visibility. When that infrastructure is strong, buyers can independently verify what they need to evaluate, budget for, and justify a product. That is buyability.

We analyzed 60 AI-native and AI-powered B2B products across five categories. The average buyability score: 55%. No company achieved full buyability. The gap between the highest and lowest scorer in the same category reached 63 points.

The patterns behind the scores matter more than the scores themselves.

The market is splitting into two camps

Across all 60 companies, one structural pattern emerged more clearly than any other. Category, company size, and brand had less predictive power than a single GTM decision: whether the company chose to make its commercial surface legible to buyers or chose to gate it behind a sales conversation.

Camp 1: Gated

Companies like Sierra, Stack AI, and Demandbase keep the commercial surface lean. No public pricing. No published value unit. Route everything through sales. Their bet: product complexity and deal size justify the gate, and the sales conversation itself is where trust gets built.

Camp 2: Buyable

Companies like Intercom, Zendesk, Zapier, Cursor, and Windsurf externalize the value unit, publish pricing, and make cost drivers legible. Their bet: the buyer, whether human or AI agent, will reward legibility with faster evaluation and higher conversion.

Neither camp has been proven definitively right. Gated companies may protect margins and control the sales narrative. Buyable companies expose themselves to comparison and price pressure. But the data reveals three structural reasons why the gap between these camps is widening.

The hidden gaps in the gated approach

Gating is a deliberate GTM choice. But it carries hidden costs that most companies are not tracking.

The trust infrastructure is strong. The buyability infrastructure lags behind.

Both Sierra and Stack AI triple down on trust, security, and compliance. Sierra claims SOC2, HIPAA, PCI DSS, ISO 27001, ISO 42001 on its home page, and documents more across its product page and a dedicated Trust Center. Stack AI does the same thing. These companies take security seriously, and it shows.

The AVS Rubric measures the full trust infrastructure: buyer-facing controls like budget caps, usage alerts, security and compliance visibility are part of it, alongside value unit clarity, cost driver mapping, and overage behavior. Sierra and Stack AI score well on the security and compliance dimensions. Where they fall short is the commercial dimensions that enable a buyer to independently build a business case. So the rubric scored their trust infrastructure as partially built, but the buyability outcome hasn't caught up.

The ROI promise draws buyers in. The missing cost architecture stalls them.

Gated companies tend to double down on measurable value promises. Stack AI's hero headline is "From process to AI agent, in minutes." Sierra leads with customer outcomes and reliability. These are compelling entry points. But when a buyer moves from "this sounds valuable" to "I need to build a business case," the surface falls short. Stack AI lists detailed cost drivers on its pricing page but offers only two tiers: Free and Enterprise (custom quote). Sierra doesn't publish a pricing page at all. The ROI promise gets the buyer interested, but without a verifiable cost architecture to match, deals stall before they reach procurement.

The commercial surface is designed to route, not to inform.

Gated companies optimize their site to generate a sales conversation. This has been the default B2B enterprise GTM playbook. But with AI-powered answer engines, a human buyer or an AI agent increasingly expects to find verifiable evidence in minutes to build a business case. If the surface gives them nothing to work with, the company simply does not show up. A GTM design decision with a measurable cost.

Why buyable companies pull ahead

Publishing the value unit is the single highest-leverage action.

Across all 60 companies, the clearest separator between top scorers and bottom scorers was whether the company had defined and published its value unit. Every top scorer had one. None of the bottom scorers did.

Intercom and Sierra both sell outcome-based AI customer support. Intercom published "$0.99 per resolution," an outcome-based model where you pay when the agent resolves the issue. Sierra describes its model as outcome-based but doesn't publish any unit definition or price. Same model, fundamentally different buyability. You can define the unit without committing to a fixed price list. The act of defining it is what closes the gap.

But how you define the value unit determines how far you go.

Salesforce Agentforce is the clearest example of a company actively moving from gated to buyable. They shipped three pricing models in eighteen months: $2 per conversation at launch (October 2024), Flex Credits at $0.10 per action (May 2025), and per-user licensing starting at $125/month (late 2025). Then in April 2026, Benioff announced Headless 360, exposing the entire Salesforce platform as APIs and MCP tools for AI agents.

Salesforce is rebuilding the commercial surface for a world where AI agents do the evaluation, going well beyond publishing a price. Their buyability score improved significantly after they moved from a "contact us" wall to published pricing. But three competing models create their own evaluation burden. A buyer still has to figure out which model applies before they can build a business case. The next step after publishing is clarity.

Self-serve companies lead, but the ceiling is broader than pricing.

The highest-scoring companies (Zapier, Cursor, Bolt, Apollo) all score between 75% and 81%. They publish clear tier pricing, documented limits, and visible cost drivers. The self-serve model forces this legibility because the product has to sell itself. Yet none of them reached full buyability. Even at the top, gaps remain in the clarity of communicating cost drivers, overage policy, operational safety rails, and enterprise trust surfaces. Most of these companies have SOC2 certification, but fewer make deeper controls visible: budget caps, usage alerts, data residency policies, audit log access, and incident response SLAs. The last mile of buyability requires the same rigor applied to pricing extended to operational controls and cost predictability.

But what about letting users in first?

Freemium is a common tactic as part of an overall acquisition program among AI-native companies. But product access and purchase justification are different problems. A user who loves your product still needs to bring a business case to finance. PLG gets the user to the product. Buyability gets the champion to the budget conversation in B2B.

The fastest fix

Most companies already have the information internally. Product and finance teams already have built the infra to operationalize the system and evolve it based on customer's usage behavioral patterns. And more importantly, they adapt it to the fast-changing business needs and new use cases. So why not externalize it as a growth lever.

Define your value unit. Publish it. Make cost drivers visible. When that gap closes, the buyer arrives decision-ready faster.

Buyability, defined and measured.

What comes next

Whether the gated approach or the buyable approach wins in the long run is still an open question. What the data shows is which direction the market is moving, and how fast. Salesforce's three-model evolution in eighteen months is one signal. Benioff rebuilding the entire platform for AI agent access is another. Zendesk and Intercom publishing outcome-based pricing in a category that was entirely gated two years ago is a third.

The full May 2026 benchmark report breaks this down across all 60 companies and 5 categories, with the patterns and opportunities we found in the data. That report is coming next.

H/T Maja Voje for the intro to the GTM Atlas by Attio.